Egypt and Angola rank among top IMF debtors

- AngolaEconomicEgypt

- November 16, 2024

Save as PDF

Save as PDFAfrican Economies Struggle with Debt Burden

Lagos, Nigeria – Five African nations feature prominently in the list of the top 10 most indebted countries to the International Monetary Fund (IMF), with Egypt and Angola leading the pack. According to data from FDI Intelligence, part of the Financial Times group, these countries illustrate the growing strain of external borrowing on Africa’s economic landscape.

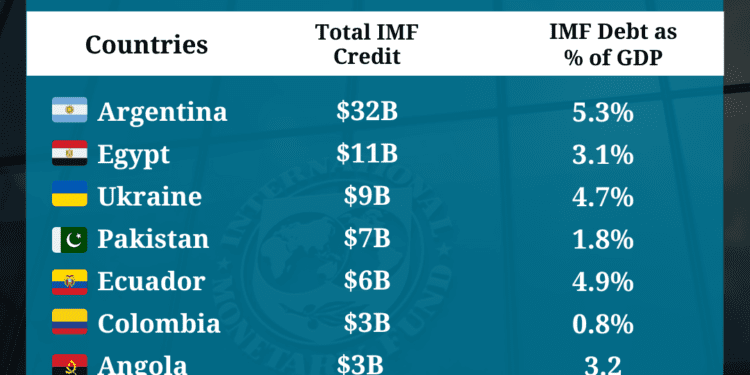

Egypt owes $14.9 billion to the IMF, making it the second-highest debtor globally, behind only Argentina’s $41 billion. This figure represents roughly 25% of all African countries’ debts to the IMF, reflecting the country’s ongoing struggle with political instability, soaring import costs, and the economic fallout of the COVID-19 pandemic.

The debt has placed significant pressure on Egypt’s economy, prompting structural adjustments, including the devaluation of its currency and subsidy reductions—measures that have drawn criticism for their impact on low-income populations.

Angola ranks seventh globally, with an IMF debt of $4.3 billion. While this amount is far below Egypt’s, it represents 6.5% of the continent’s total obligations to the IMF. The debt reflects Angola’s efforts to stabilize its economy after years of dependence on oil exports and price volatility in global markets.

The Angolan government has initiated reforms to diversify its economy, but progress has been slow, leaving the country reliant on external borrowing to bridge fiscal gaps.

In addition to Egypt and Angola, three other African nations are listed among the IMF’s most indebted countries:

- Kenya: $3.4 billion (8th place)

- South Africa: $3 billion (9th place)

- Ghana: $2.74 billion (10th place)

Combined, these five nations account for $28.34 billion, or approximately 19% of the IMF’s total global lending, which currently stands at $149 billion.

Globally, the largest IMF debtors include countries such as Ukraine ($12 billion), Pakistan ($7.72 billion), and Ecuador ($6.69 billion). While African countries’ debt levels are comparatively lower, the conditions attached to IMF loans—such as fiscal austerity and currency devaluations—disproportionately affect their economic stability and growth potential.

Economists point out that African nations face unique challenges with IMF borrowing:

- Diversification gaps: Many economies remain heavily reliant on commodity exports, making them vulnerable to price shocks.

- Austerity measures: Loan conditions often force governments to reduce public spending, exacerbating social inequality.

- Limited alternatives: With restricted access to global credit markets, countries often have no choice but to turn to the IMF.

To reduce dependence on external borrowing, analysts recommend:

- Expanding investments in renewable energy, technology, and manufacturing.

- Enhancing fiscal discipline by improving tax collection systems and curbing wasteful spending.

- Strengthening regional cooperation through organizations like the African Union to negotiate better financing terms.

As Egypt and Angola navigate their IMF obligations, their experiences serve as a cautionary tale for other African economies. While external borrowing offers short-term relief, it underscores the need for long-term strategies to build economic resilience and reduce dependence on international creditors.