Cobalt, value chains and power, Africa and the new industrial order of energy

- Business and NetworkingCentral AfricaDemocratic Republic of the Congo (DRC)

- March 30, 2026

Save as PDF

Save as PDFJohannesburg – The global energy transition is reshaping not only markets but also the balance of economic power. At the centre of this transformation lies cobalt, a critical mineral whose geography is dominated by the Democratic Republic of Congo (DRC), which accounts for roughly 70 per cent of global supply. Yet the country captures less than 10 per cent of the total value generated across the global supply chain.

AfricaHeadline Reports Team

editorial@africaheadline.com

This imbalance reflects a deeper structural reality. In 2025, the global battery market surpassed $180bn, with projections pointing to more than $400bn by 2030. However, most of this value is generated outside Africa. The DRC remains largely confined to exporting raw or semi-processed materials, while refining, chemical processing and battery manufacturing are concentrated in more industrialised economies.

China holds a commanding position in this chain. It controls approximately 75 per cent of global cobalt refining capacity and maintains significant stakes in several Congolese mining operations. Further downstream, companies based in China, South Korea and Japan account for more than 80 per cent of global battery cell production, reinforcing a highly integrated industrial ecosystem.

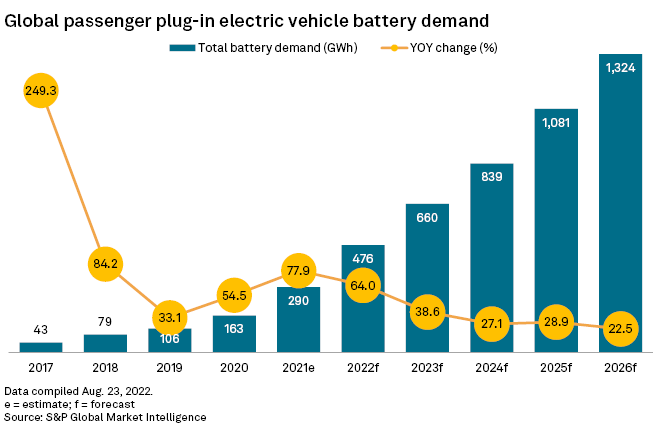

Demand is rising rapidly. Global electric vehicle sales exceeded 14mn units in 2025, representing around 18 per cent of total car sales. Forecasts suggest this could reach between 40mn and 45mn units by 2030, lifting market share to more than 40 per cent. As a result, demand for critical minerals, including cobalt, lithium and nickel, is expected to grow between three and five times over the next decade.

In this context, cobalt has become a geopolitical asset. The United States has mobilised roughly $369bn through the Inflation Reduction Act to strengthen domestic supply chains and accelerate clean energy deployment. The European Union, through its Critical Raw Materials Act, aims to reduce external dependencies and secure access to strategic inputs. China, meanwhile, has consolidated its position over the past decade through sustained investment in African mining, logistics and refining.

The DRC now sits at the heart of this global competition. With reserves estimated at more than 3.5mn tonnes, the country holds a unique strategic advantage. Yet it continues to face structural constraints, including limited infrastructure, low levels of industrialisation and governance challenges.

Artisanal mining remains a significant component of output, accounting for up to 30 per cent of production and involving more than 200,000 workers. Much of this activity operates outside formal regulatory frameworks, limiting fiscal revenues and raising concerns around environmental, social and governance standards. In a market increasingly shaped by ESG requirements, these issues have direct implications for competitiveness.

There are, however, early signs of repositioning. Regional initiatives between the DRC and Zambia aim to develop a battery value chain, while investments linked to the Lobito Corridor, estimated at over $1bn, are designed to improve transport links between mining regions and export routes.

Despite these developments, Africa’s refining capacity remains limited, accounting for less than 5 per cent of the global total. The bulk of value creation continues to take place elsewhere, reinforcing external dependence.

Indonesia’s experience in the nickel sector offers a useful precedent. By restricting raw exports and mandating local processing, the country attracted more than $30bn in industrial investment and rapidly moved up the value chain. A similar strategy applied to cobalt could significantly reshape the DRC’s economic trajectory.

The future of the cobalt value chain is likely to follow one of three paths. In a baseline scenario, Africa remains a supplier of raw materials with limited gains. In an intermediate scenario, investment in refining and processing could double or triple revenues. In a more ambitious scenario, the development of a regional battery industry could increase value capture by five to ten times.

Strategically, the picture is clear. The DRC holds dominant reserves and a central role in the global energy transition. Yet structural weaknesses constrain its ability to capture value. At the same time, rising demand and shifting geopolitics create a window of opportunity, even as risks such as technological substitution and price volatility remain.

Cobalt is no longer just a commodity. It is a lever of economic power.

The question is whether Africa will remain at the base of the value chain or emerge as one of its industrial centres.

AfricaHeadline Intelligence | Strategic Insight Unit

Global Economics | Geopolitics | Africa Transformation