Africa’s Inflation battle enters a new phase as price pressures ease unevenly across the continent

- Economic

- June 29, 2026

Save as PDF

Save as PDFFalling inflation is improving the outlook for investors, but Nigeria, Egypt and Angola remain among Africa’s highest-inflation economies

JOHANNESBURG — Africa’s fight against inflation is beginning to yield results. After three years of sharp price increases triggered by the pandemic, the war in Ukraine, aggressive global monetary tightening and a stronger U.S. dollar, several of the continent’s largest economies are finally seeing inflation moderate in 2026.

The improvement, however, is far from uniform. While a handful of economies have returned to relative price stability, others continue to grapple with double-digit inflation, currency volatility and structural supply constraints, underscoring the uneven pace of Africa’s macroeconomic recovery.

According to the International Monetary Fund (IMF), global inflation is projected to average 3.8% in 2026, while the average across Africa’s ten largest economies remains close to 10%, more than double the global rate. The gap highlights the continent’s continued exposure to imported inflation, food and energy dependence, exchange-rate volatility and elevated borrowing costs.

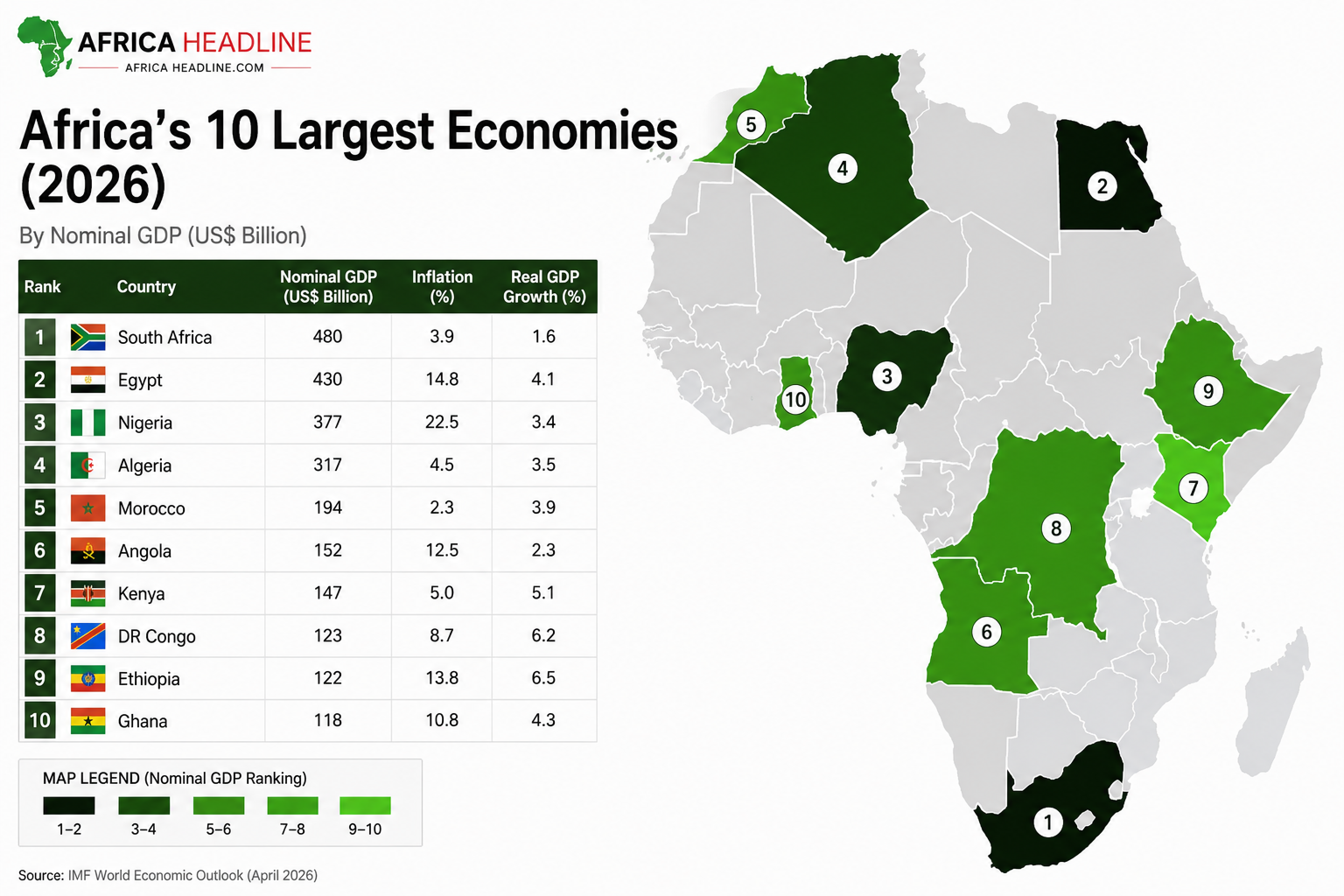

Africa’s largest economies in 2026

Table 1 | GDP, Economic Growth and Inflation

| Rank | Country | Nominal GDP (US$ bn) | GDP Growth (%) | Inflation (%) |

|---|---|---|---|---|

| 1 | South Africa | 480 | 1.8 | 3.9 |

| 2 | Egypt | 430 | 4.1 | 14.8 |

| 3 | Nigeria | 377 | 3.2 | 22.5 |

| 4 | Algeria | 317 | 3.5 | 4.6 |

| 5 | Morocco | 194 | 3.9 | 2.3 |

| 6 | Angola | 152 | 2.3 | 12.4 |

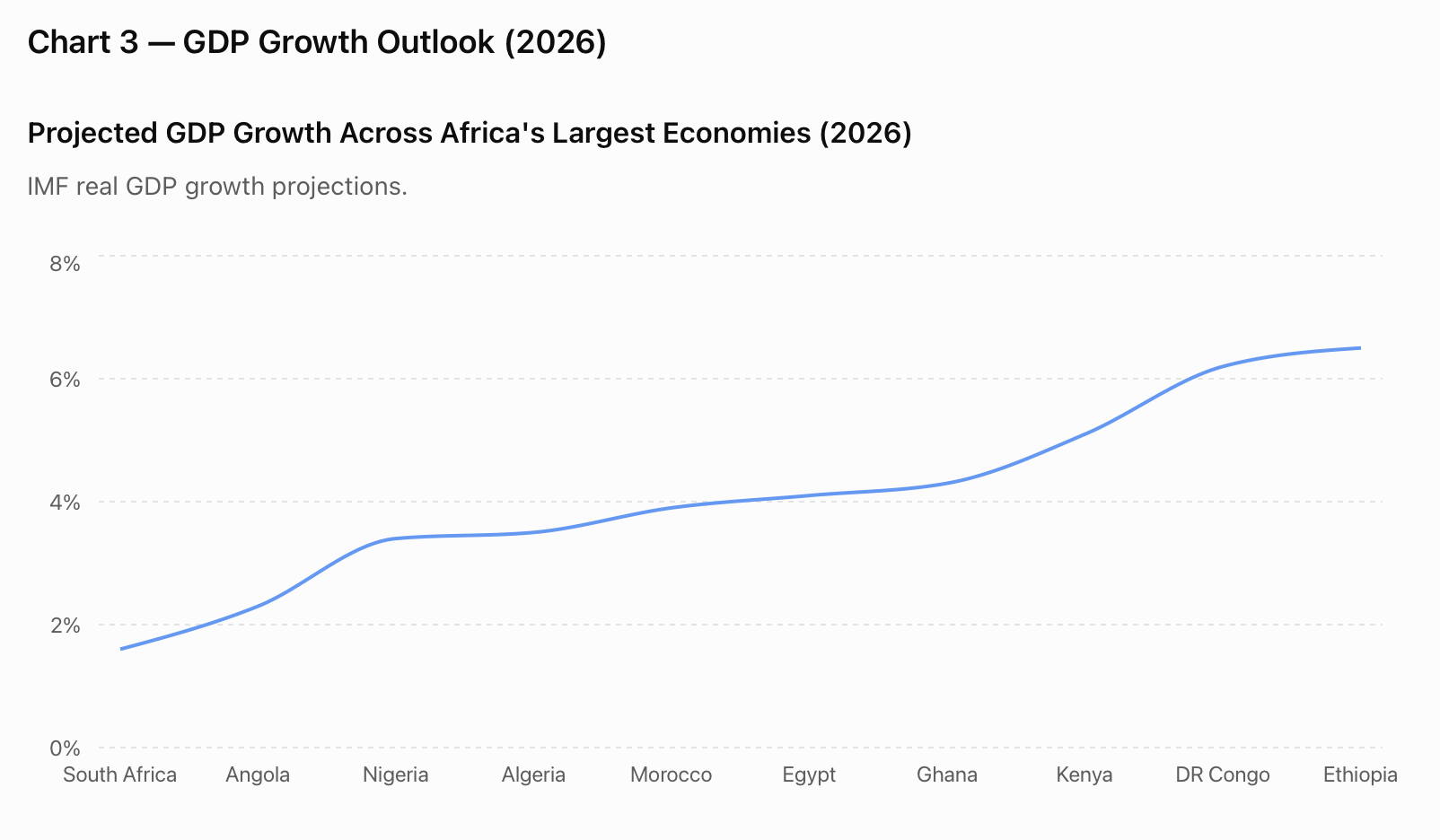

| 7 | Kenya | 147 | 5.0 | 5.0 |

| 8 | DR Congo | 123 | 6.1 | 8.6 |

| 9 | Ethiopia | 122 | 6.5 | 13.8 |

| 10 | Ghana | 118 | 4.2 | 10.9 |

Source: International Monetary Fund, World Economic Outlook 2026.

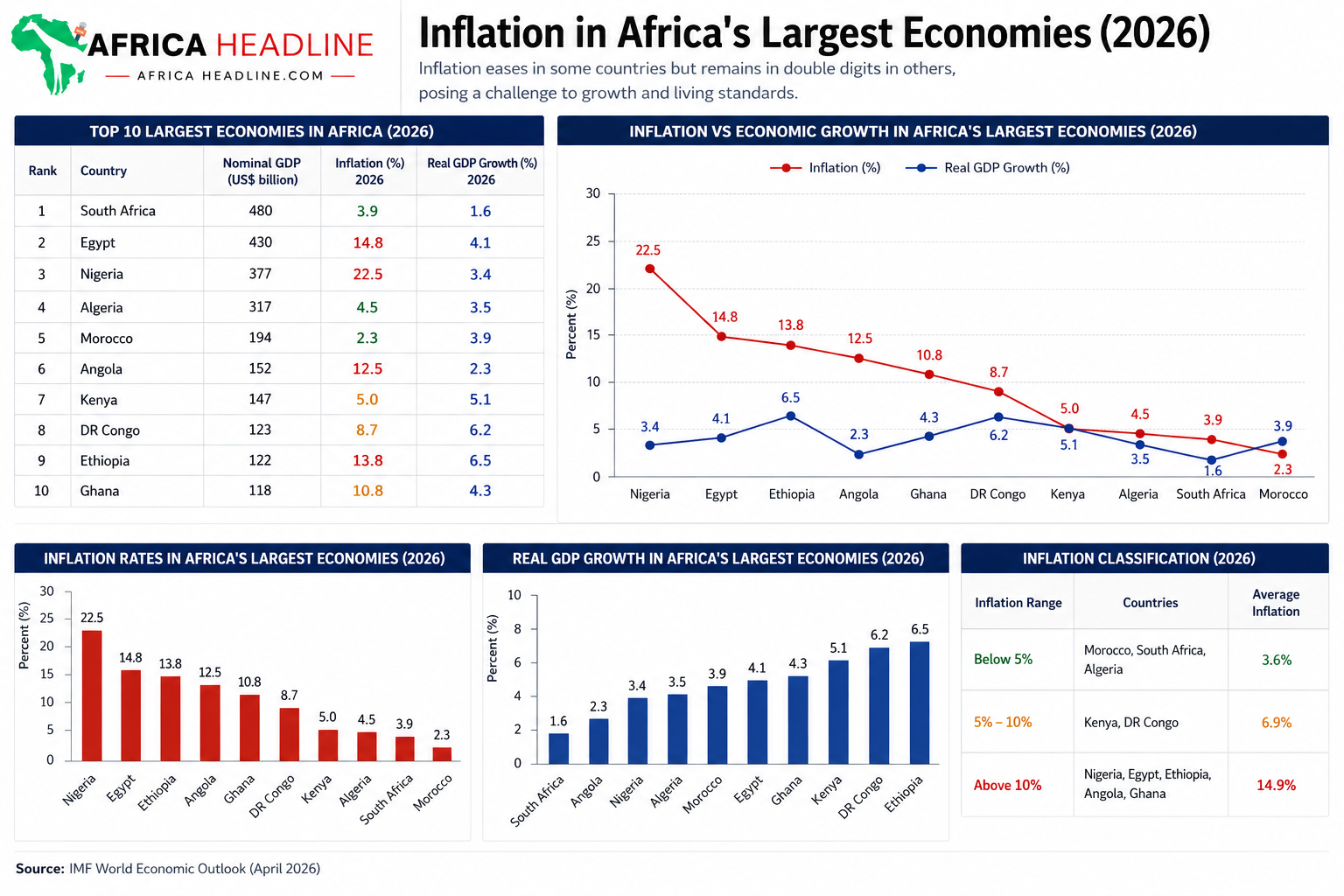

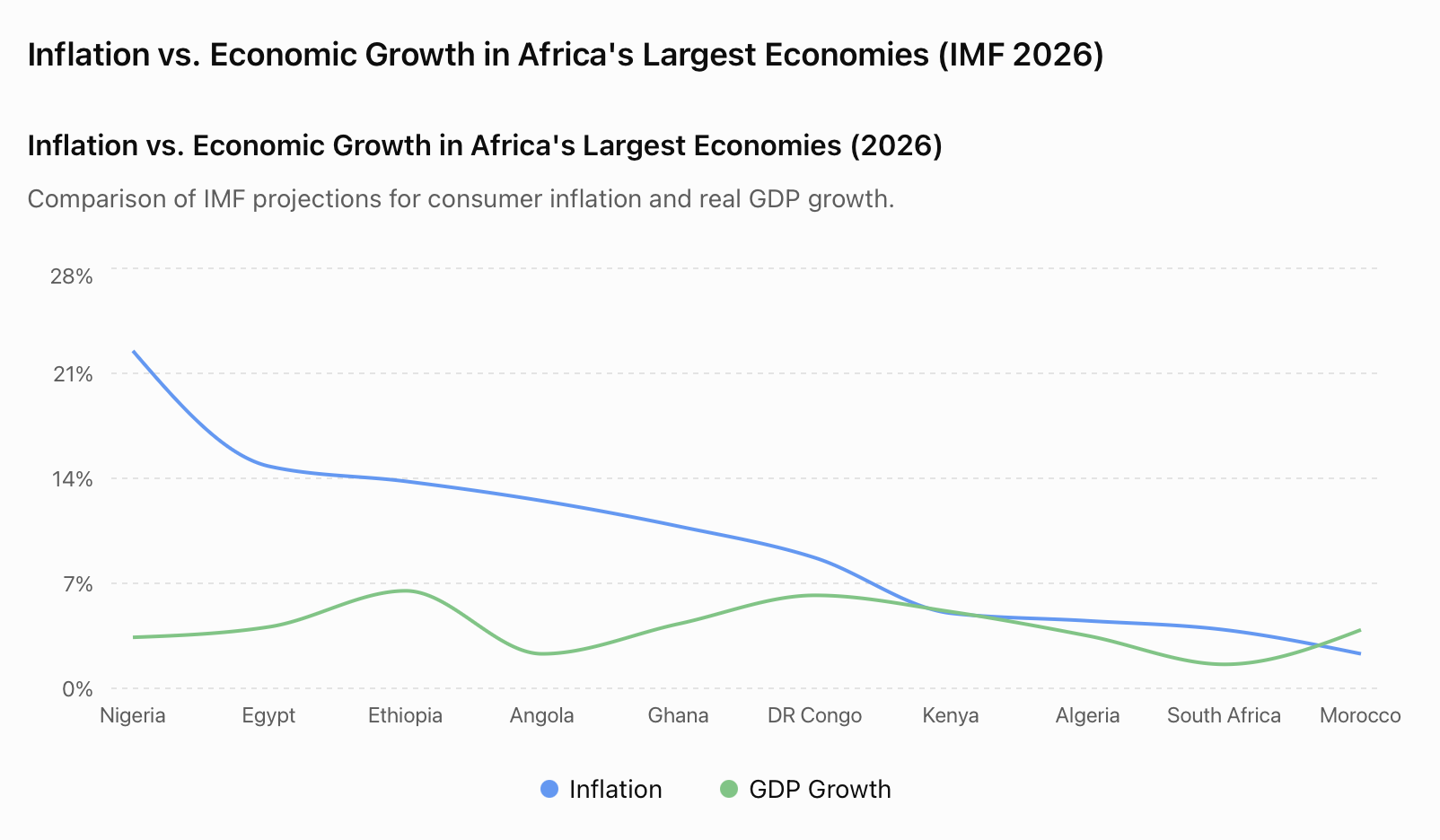

Inflation across Africa’s largest economies

A continent recovering at two speeds

The IMF projections paint a picture of an increasingly divided continent.

Morocco, South Africa and Algeria have largely restored price stability, maintaining inflation below 5% through credible monetary policy, relatively stable exchange rates and stronger domestic financial systems.

At the opposite end of the spectrum sits Nigeria, where inflation is expected to remain above 22%, the highest among Africa’s major economies. Currency liberalisation, the removal of fuel subsidies and persistent weakness in the naira continue to fuel consumer prices despite ongoing economic reforms.

Egypt is forecast to record inflation close to 15%, reflecting the lingering effects of repeated currency devaluations and IMF-backed structural reforms aimed at restoring macroeconomic stability.

Meanwhile, Ghana, Ethiopia, Democratic Republic of Congo and Kenya occupy the middle ground, with inflation easing but remaining vulnerable to global commodity prices and currency fluctuations.

Angola emerges as one of Africa’s fastest disinflation stories

Among Africa’s largest economies, Angola has recorded one of the continent’s sharpest declines in inflation.

Consumer price growth has fallen from around 20% in mid-2025 to approximately 12.4% in 2026, representing a decline of more than seven percentage points in less than twelve months.

The improvement reflects a combination of tight monetary policy by the National Bank of Angola, greater exchange-rate stability, improved fiscal discipline and slower growth in domestic liquidity.

Although inflation remains above regional averages, Angola’s rapid disinflation places it among the strongest macroeconomic performers in Sub-Saharan Africa over the past year.

The IMF forecasts Angola’s economy will expand by 2.3% in 2026, supported by a gradual recovery in the non-oil sector and rising private investment.

GDP growth forecast (2026)

Markets shift their focus beyond Inflation

For investors, moderating inflation represents more than an improvement in consumer purchasing power—it signals the beginning of a new investment cycle.

Lower inflation reduces sovereign borrowing costs, eases pressure on interest rates, supports corporate financing and improves debt sustainability, making African assets increasingly attractive after several years of macroeconomic instability.

However, investors remain cautious. Currency volatility, geopolitical tensions, commodity price swings and fiscal consolidation will continue to shape investment decisions across the continent.

Countries capable of maintaining macroeconomic discipline while accelerating structural reforms are expected to attract the largest share of foreign direct investment, particularly in energy, mining, agriculture, digital infrastructure and manufacturing.

Table 2 | Macroeconomic comparison

| Country | Inflation | GDP Growth | Economic Outlook |

|---|---|---|---|

| Morocco | 2.3% | 3.9% | Highly stable |

| South Africa | 3.9% | 1.8% | Stable |

| Algeria | 4.6% | 3.5% | Stable |

| Kenya | 5.0% | 5.0% | Strong growth |

| DR Congo | 8.6% | 6.1% | Rapid expansion |

| Ghana | 10.9% | 4.2% | Gradual recovery |

| Angola | 12.4% | 2.3% | Rapid disinflation |

| Ethiopia | 13.8% | 6.5% | High inflation |

| Egypt | 14.8% | 4.1% | Economic adjustment |

| Nigeria | 22.5% | 3.2% | Severe inflation pressures |

Inflation vs Economic growth

Outlook, From Inflation control to sustainable growth

For much of the past three years, inflation has dominated Africa’s economic agenda. That narrative is now beginning to change.

If governments maintain fiscal discipline, preserve central bank credibility and accelerate structural reforms, 2026 could mark the turning point from inflation management to sustainable economic expansion.

The next phase of Africa’s growth story will be determined less by commodity prices and more by productivity gains, industrial diversification, infrastructure investment and institutional credibility.

For global investors, the question is no longer whether inflation will fall, but which African economies will successfully transform macroeconomic stability into long-term, investment-led growth.

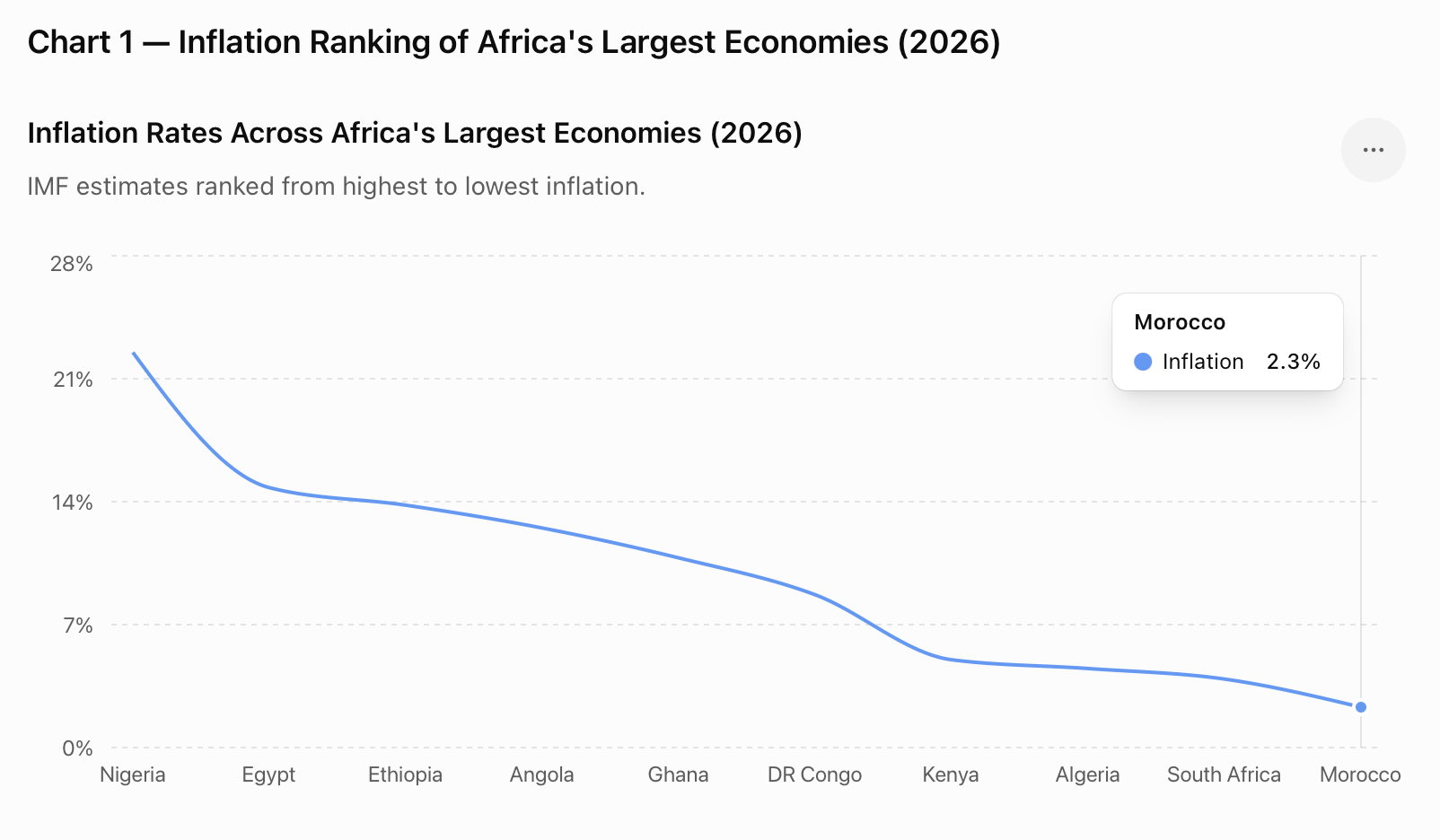

IMF projections for 2026.

| country | inflation |

|---|---|

| Nigeria | 22.5 |

| Egypt | 14.8 |

| Ethiopia | 13.8 |

| Angola | 12.4 |

| Ghana | 10.9 |

| DR Congo | 8.6 |

| Kenya | 5 |

| Algeria | 4.6 |

| South Africa | 3.9 |

| Morocco | 2.3 |

IMF projections for 2026.

| country | growth |

|---|---|

| Ethiopia | 6.5 |

| DR Congo | 6.1 |

| Kenya | 5 |

| Ghana | 4.2 |

| Egypt | 4.1 |

| Morocco | 3.9 |

| Algeria | 3.5 |

| Nigeria | 3.2 |

| Angola | 2.3 |

| South Africa | 1.8 |

Africa’s largest economies in 2026.

| country | inflation | growth |

|---|---|---|

| Nigeria | 22.5 | 3.2 |

| Egypt | 14.8 | 4.1 |

| Ethiopia | 13.8 | 6.5 |

| Angola | 12.4 | 2.3 |

| Ghana | 10.9 | 4.2 |

| DR Congo | 8.6 | 6.1 |

| Kenya | 5 | 5 |

| Algeria | 4.6 | 3.5 |

| South Africa | 3.9 | 1.8 |

| Morocco | 2.3 | 3.9 |

Africa’s inflation outlook in 2026 reflects a continent moving at two different speeds. While countries such as Morocco, South Africa and Algeria have largely restored price stability with inflation below 5%, major economies including Nigeria, Egypt, Angola, Ethiopia and Ghana continue to struggle with double-digit inflation driven by currency depreciation, high import costs and structural supply constraints.

Despite these differences, the overall trend points toward moderating inflation across the continent, suggesting that the worst of the recent inflationary cycle may be over. The next challenge for African policymakers will be to translate lower inflation into stronger, more inclusive economic growth by accelerating structural reforms, boosting domestic production and attracting long-term investment.

For investors, countries that successfully combine declining inflation with sustained GDP growth are likely to emerge as Africa’s most attractive destinations over the coming years.